In today’s volatile economic climate, making the most of our hard-earned money is more important than ever. When the bulk of our waking hours are spent working for that paycheck, it’s worth our while to spend some time and effort thinking about how to stretch our dollars and make the most of our savings. As a financially savvy Singaporean (since you’re reading this, I’m assuming you’re one of us!) constantly seeking ways to grow your savings, whether through high-yield savings accounts or innovative financial products, is almost akin to a rite of passage to true adulthood and financial freedom.

So today, let’s talk about savings accounts: Singlife interest vs. traditional savings accounts— which offers better returns?

If you’ve been searching for the best interest rates in Singapore or wondering how to achieve financial flexibility while earning significant returns, this article will guide you through the pros and cons of both options and help you to decide the best way to stretch your savings.

The Singlife Account: A Game-Changer in Personal Finance

What Is the Singlife Account?

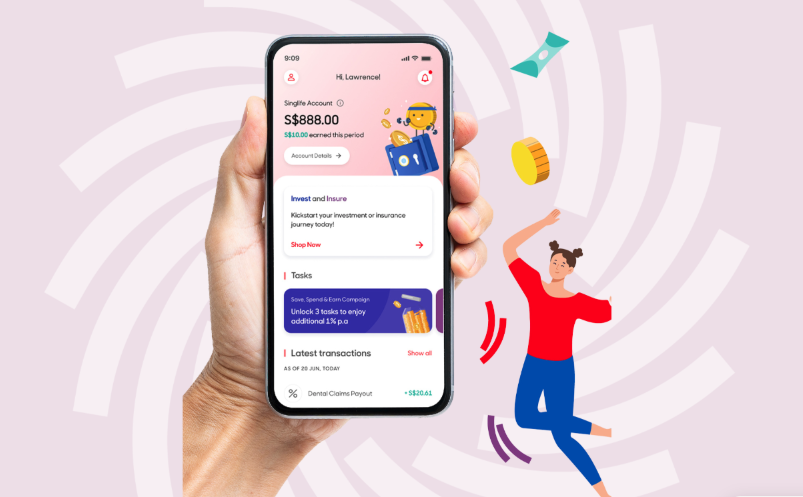

The Singlife Account is a revolutionary savings product offering attractive interest rates with no lock-in periods or penalties for withdrawals. Designed to provide both flexibility and returns, the account is ideal for Singaporeans looking to earn up to 4.5% p.a. on their savings while enjoying additional benefits like life insurance coverage.

Key Features:

1. Base Interest Rates

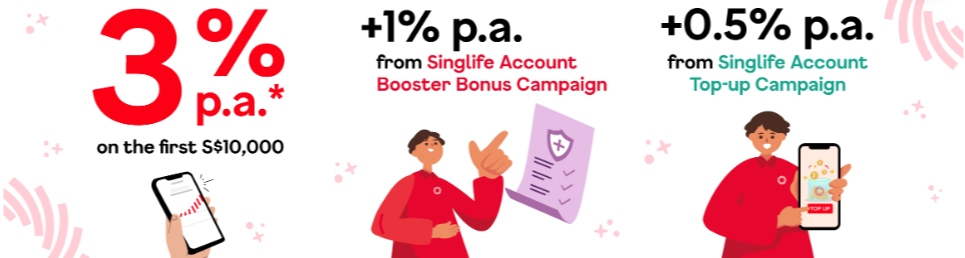

- 3% p.a. on the first S$10,000.

- 1% p.a. on amounts between S$10,000 and S$100,000.

- No interest on balances exceeding S$100,000

2. Bonus Campaigns for Enhanced Returns

- Top-up Bonus: Earn an extra 0.5% p.a. on the first S$10,000 by topping up at least S$800 during promotional periods.

- Booster Bonus: An additional 1% p.a. is available for customers purchasing eligible Singlife Life or Health insurance policies.

3. Life Insurance Coverage

Singlife Account holders automatically receive life insurance coverage of up to 105% of their account value, ensuring peace of mind alongside competitive returns.

4. No Hidden Fees

Unlike some traditional accounts, there are no lock-in periods or penalties for withdrawals, making the Singlife Account a truly flexible option.

Traditional Savings Accounts in Singapore

Traditional savings accounts have long been the go-to choice for Singaporeans. Offered by established banks like DBS, OCBC, and UOB, these accounts provide a secure place to store your money while earning modest interest. However, their returns often depend on meeting specific conditions.

Key Features:

1. Base Interest Rates:

Typically range from 0.05% to 0.5% p.a., which is significantly lower than the Singlife Account.

2. Bonus Interest Programs:

Many banks offer higher interest rates (up to 2%–7% p.a.) for customers who:

- Credit their salary to the account.

- Meet a minimum spending threshold on their credit card.

- Purchase investment or insurance products.

- Take up loans or make bill payments through the bank.

3. Complex Conditions

While bonus programs can boost returns, they often involve multiple conditions that must be met consistently. Failing to do so reduces the effective interest rate. For instance, Bank of China’s Smart Saver Account has the highest interest rate at 7%. However, achieving the 7% interest rate involves:

- Purchasing eligible insurance products for at least 12 months

- Spending at least $500 on your debit or credit card in a calendar month

- Spending at least $1500 on your debit or credit card in a calendar month

- Crediting at least $2000 to $6000 of your monthly salary every month

- Crediting at least $6000 of your monthly salary every month

- Completing at least 3 bill payments via internet banking, mobile banking or GIRO

- Fulfilling any of the above requirements for payment bonus interest, card spend or salary crediting

4. Limited Flexibility

With some savings programs, withdrawals or missed criteria can reset your bonus interest, making it harder to maximise returns.

Comparing Singlife and Traditional Savings Accounts

1. Interest Rates

- Singlife offers up to 4.5% p.a. on the first S$10,000, far exceeding the base rates of traditional accounts.

- Traditional accounts may offer higher returns on balances above S$10,000, provided bonus conditions are met.

2. Accessibility and Simplicity

- Singlife’s straightforward structure makes it easy for users to earn high returns without juggling multiple criteria.

- Traditional accounts require customers to navigate complex programs, often tying their financial behaviour to specific banks.

3. Additional Benefits

- Singlife includes life insurance coverage, adding value beyond just savings growth.

- Traditional accounts generally do not offer complementary insurance.

4. Withdrawal Flexibility

- Singlife allows penalty-free withdrawals at any time, ensuring financial flexibility.

- Some traditional accounts penalise withdrawals by reducing or nullifying bonus interest.

Why Singlife May Be the Smarter Choice

For many Singaporeans, the Singlife Account stands out as the smarter choice for savings due to its combination of flexibility, simplicity, and high returns. Here’s why:

1. Maximised Returns for Lower Balances:

If your savings are under S$10,000, Singlife provides unparalleled returns of up to 4.5% p.a., outperforming traditional banks.

2. No Strings Attached

Unlike traditional accounts, Singlife doesn’t burden you with complex bonus conditions. You earn rewards simply by saving and maintaining your balance.

3. Insurance Protection

The added life insurance coverage ensures that your loved ones are financially secure in case of unforeseen events.

4. Perfect for Savvy Savers

Singlife’s innovative model is designed for modern savers seeking both growth and flexibility.

Who Should Consider Traditional Savings Accounts?

While Singlife offers excellent benefits, traditional savings accounts may still appeal to certain segments:

1. High-Balance Savers

If you maintain balances exceeding S$10,000, traditional accounts might offer more competitive rates, provided you meet their conditions.

2. Integrated Banking Needs:

Customers already entrenched in a bank’s ecosystem (e.g., salary crediting, mortgage loans) may find it easier to meet bonus conditions and maximise returns.

Final Verdict: Singlife Interest vs. Traditional Savings Accounts

For Singaporeans with savings under S$10,000 or those seeking a simple, flexible way to grow their money, the Singlife Account is hard to beat. Its combination of high interest rates, flexibility, and added insurance benefits makes it an ideal choice for those wanting to make the most of their savings.

On the other hand, if you’re comfortable managing the complexities of bonus interest programs and maintain larger balances, traditional savings accounts may offer better returns over the long term.

Make Your Savings Work for You

Ready to take the next step? Open a Singlife Account today and start enjoying competitive interest rates, financial flexibility, and peace of mind. With Singlife, growing your savings has never been easier.